From Balance Sheets to Blockchains

If 2024 was about ETFs opening the door to TradFi, 2025 was the year digital asset treasuries became mainstream, as the MicroStrategy playbook evolved from an outlier into an industry standard. Public companies across the U.S. and abroad began actively converting cash reserves into crypto, with firms like Semler Scientific and Metaplanet leveraging debt and equity issuance to accumulate bitcoin and report BTC yield as a core metric, while Bitmine Immersion Technologies and DeFi Development Corp extended the model into Ethereum staking and DeFi-native “active treasuries.” At the same time, ETFs shifted from simple access products to utility-driven vehicles, with staking-enabled Solana ETFs, DeFi-powered yield ETFs, and multi-asset crypto index funds bringing onchain economics into familiar wrappers. Together, corporate balance sheet adoption and increasingly sophisticated ETF structures cemented digital assets as a permanent pillar of global finance, while still hinting at how much further the model can evolve.

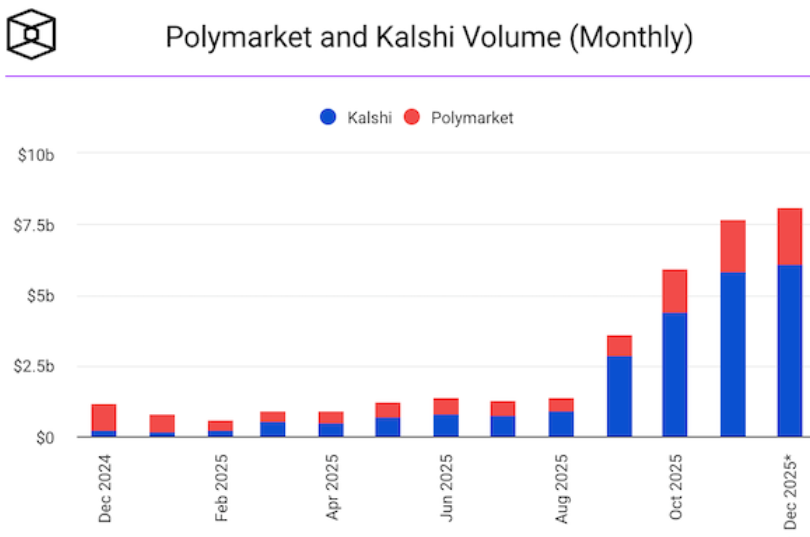

Prediction Markets Go Vertical

Prediction markets emerged as one of the year’s standout sectors, generating over $32 billion in trading volume as activity accelerated sharply in the back half of the year. After a flat H1, volumes surged from September through December, with Polymarket tripling and Kalshi growing fivefold, pushing prediction markets’ share of CEX spot volume from 0.03% to 0.73%. While Kalshi now claims roughly 75% of volume based on self-reported data and Polymarket trails with fully onchain, verifiable figures, both platforms have seen steady growth in open interest, which now exceeds $690 million combined and is approaching prior cycle highs.

Source: Kalshi, The Block

Stablecoins Grow Up

The passage of the GENIUS Act in July gave stablecoins clear federal rules and ended regulation by enforcement, unlocking rapid commercial adoption as institutions like Visa, PayPal, and major asset managers scaled settlement and tokenized funds with confidence. Stablecoins cemented their role as core financial infrastructure in 2025, surpassing $300B in market cap and settling trillions onchain, dominated by USDT and USDC and increasingly distributed through consumer wallets like MetaMask and Phantom. Experimentation accelerated around yield, with high-growth but volatile models like Ethena’s USDe contrasting with more conservative Treasury-backed designs, while new infrastructure emerged to support payments, settlement, and composable yield. Together, regulatory clarity and real-world usage shifted stablecoins from speculative instruments to indispensable rails for global onchain finance.

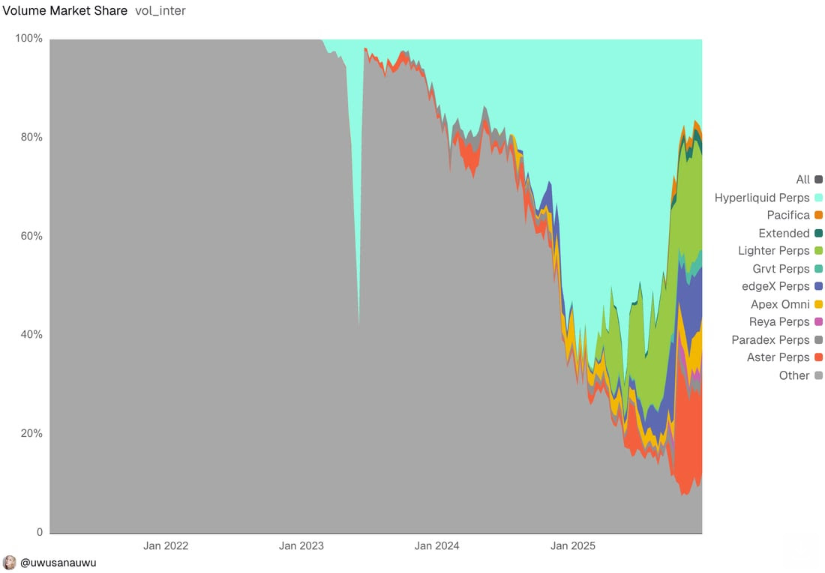

Perps Go Onchain, Then Go Competitive

Decentralized perpetuals became one of crypto’s clearest product-market-fit stories in 2025, processing over $6.9 trillion in volume as the DEX-to-CEX futures ratio more than tripled to 17%, reflecting a sustained shift toward self-custodial, frictionless trading. Hyperliquid defined the category early, setting benchmarks in volume, revenue, liquidity, and wallet distribution, while evolving into a gravity well for stablecoin issuers and onchain liquidity. By Q4, however, rising competitors like Lighter and Aster broke its dominance, pushing the market into an oligopoly where traders rotate based on incentives and fees rather than platform loyalty, signaling the sector’s transition from breakout success to mature, competitive infrastructure.

Source: Dune

Great Products, Terrible Charts

Despite 2025 being billed as a breakout year for crypto, most altcoins severely underperformed both Bitcoin and traditional assets, with the S&P 500 up 17%, BTC down 6%, and the altcoin-heavy “Others” index down 43%. Even established names like LINK and AAVE remain far below prior highs, while last cycle’s speculative winners such as DOT have been nearly wiped out. More strikingly, tokens from strong, fast-growing protocols like Ethena and Pump.fun also collapsed, down roughly 78% despite clear usage and record TVL. While capital continues flowing onchain via stablecoins and RWAs, liquid risk appetite for altcoins has largely evaporated, leaving most holders deep underwater.

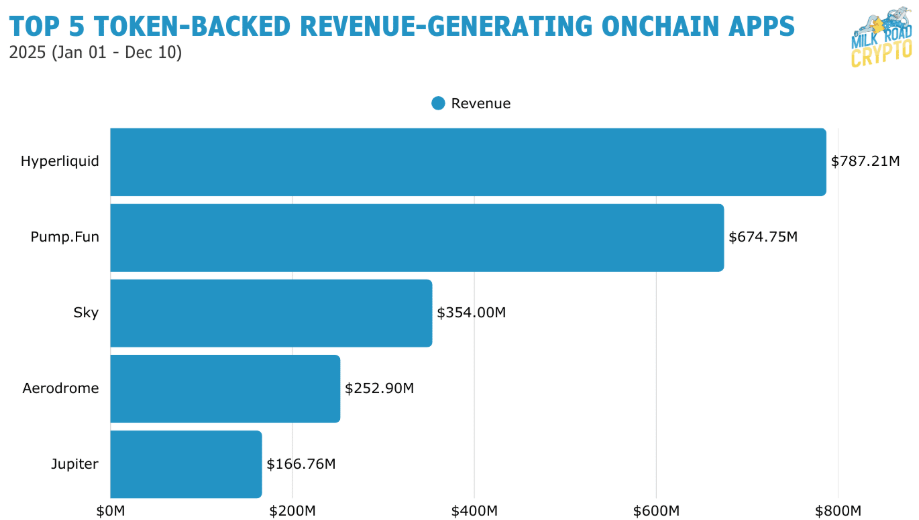

Follow the Fees

Revenue once again proved to be one of the clearest signals of real onchain usage in 2025, with Hyperliquid ($787M), Pump.fun ($675M), Sky ($354M), Aerodrome ($253M), and Jupiter ($167M) emerging as the top token-backed revenue generators of the year based on Artemis and Blockworks data through December 10. While these protocols dominated activity across perps, launchpads, yield, and DEX trading, token performance varied widely, underscoring a growing disconnect between fundamentals and price. Pump.fun and Hyperliquid delivered outsized gains at peak, while others posted far more modest returns despite strong cash flow, reinforcing that revenue is a necessary but no longer sufficient condition for token outperformance in a more mature market.

Source: Artemis, Blockworks, Milk Road

Important Legal Notices

This reflects the views MJL Capital LLC (“MJL”), but it should in no way be construed to represent financial or investment advice. Nothing in this correspondence is intended to constitute or form part of, and should not be construed as, an issue for sale or subscription of, or solicitation of any offer or invitation to subscribe for, underwrite, or otherwise acquire or dispose of any security, including any interest in any private investment fund managed by MJL. Any such offer may only be made pursuant to a formal confidential private placement memorandum of any such fund, which may be furnished to potential investors upon request and which will contain important information to be considered in connection with any such investment, including risk factors associated with making any investment in any such fund. Further, nothing in this correspondence is, or is intended to be treated as, investment or tax advice. Each recipient should consult their own legal, tax and other professional advisors in connection with investment decisions.

Domenic Salvo is a Managing Partner at MJL Capital, helping lead Portfolio Research and Investor Relations.